Buying property in Boston means entering one of the most expensive and competitive housing markets in the country. The median home price in Boston sits around $837,000 as of mid-2025, roughly double the national median. Single-family homes inside city limits averaged $1.31 million in 2025, a 15.7% jump from the year before (Dwell360 Market Report, March 2026). That’s not a typo. And yet, Boston keeps attracting buyers because the fundamentals hold up: low vacancy, steady rent growth, a property tax rate that’s still below many peer cities, and an economy anchored by world-class universities and hospitals that aren’t going anywhere.

This isn’t a city where you buy on a whim. It rewards preparation and punishes guesswork. I’ve watched buyers lose $30,000 in a single weekend by skipping inspections to win a bidding war. So here’s what you actually need to know before you write that offer.

This article won’t cover commercial real estate, short-term rental regulations (which deserve their own deep dive), or suburban markets outside Route 128. We’re focused on residential purchases inside Boston proper.

What does buying property in Boston cost in 2026? The citywide median sale price is approximately $837,000, with single-family homes averaging $1.31 million and condos around $866,000 (Greater Boston Housing Report Card 2025, Boston Foundation). Closing costs typically run 1.25% to 2.44% of the purchase price, and the FY2026 residential property tax rate is $12.40 per $1,000 of assessed value.

Why Is Buying Property in Boston Still a Smart Move?

Boston’s economy doesn’t depend on one industry. That’s the single biggest reason the housing market here doesn’t crater the way markets in single-industry cities do. Biotech, higher education, healthcare, finance, and tech all compete for talent in this city. Harvard, MIT, Massachusetts General Hospital, and dozens of biotech firms create a floor under housing demand that most US metros can’t match.

The city is also physically small. Boston covers just 89 square miles, and much of the housing stock is 75+ years old. You can’t bulldoze Beacon Hill to build condos. That constraint on supply is a feature for buyers, not a bug. It means your property doesn’t compete with endless new construction the way homes in Phoenix or Austin do.

And here’s something most people overlook: Boston’s public transit system makes it one of the few US cities where you can live comfortably without a car. That reduces total cost of living and broadens the pool of renters for investment properties. According to the Joint Center for Housing Studies at Harvard, the Northeast saw 6.8% annual home price growth in Q1 2025, the strongest of any US region.

One contrarian take: the “wait for rates to drop” crowd is probably wrong on Boston. Mortgage rates in the high-6% range feel painful compared to the 3% era, but the long-term average since 1971 is 7.73% (Freddie Mac data). We’re not in crisis territory. We’re in normal territory. And every month you wait, Boston’s constrained supply keeps prices from falling in any meaningful way.

What Does the Boston Property Market Look Like in 2026?

The short answer: prices have stabilized after two years of sharp gains, inventory is slowly rising, and buyers have more negotiating room than they’ve had since 2019. It’s not a buyer’s market. But it’s not the frenzy of 2022 either.

How Strong Is Boston’s Rental Demand?

Very strong. Average effective rents rose 2.3% year over year in 2024, well above the national average of 1.0%. Occupancy rates held at roughly 96.5% through Q4 2024. Boston absorbed over 1,300 new rental units in Q1 2025 alone, with another 1,851 absorbed in Q2. The city added about 7,200 new rental units in 2024 and expects around 7,000 more in 2025. That’s only 2.6% of total inventory, right in line with historical averages. Average rent in Boston is roughly $3,478 per month, about 70% higher than the national average (Zillow, 2025).

For buyers considering rental income, this matters. Vacancy risk in Boston is among the lowest in the country. The steady stream of students, medical professionals, and tech workers means you’re not gambling on tenant demand the way you would in a market that boomed purely on pandemic migration.

How High Are Boston Home Prices Right Now?

It depends heavily on what you’re buying and where.

| Property Type / Area | Median/Avg Price | YoY Change | Source |

| Boston Single-Family (City) | $1,312,308 avg | +15.7% | Dwell360, Mar 2026 |

| Boston Single-Family (Median) | $837,287 | +5.3% | Boston Foundation, 2025 |

| Boston Condo (Median) | ~$866,074 | Varies | Boston Foundation, 2025 |

| Greater Boston Metro | $802,000 | -6.2% | Redfin, Feb 2026 |

| National Median (Existing) | $412,500 | +4.2% | JCHS/NAR, 2024 |

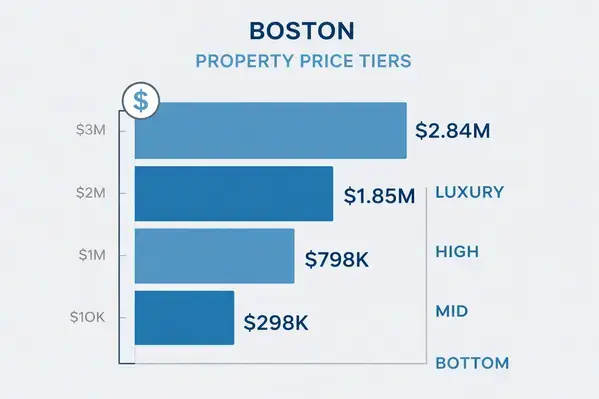

| Bottom Tier (Boston) | ~$298,000 | N/A | Redfin Tiers, 2026 |

| Luxury Tier (Boston) | $1.18M–$2.84M+ | N/A | Redfin Tiers, 2026 |

Notice the gap between the city average and metro median. That $500,000 spread tells you everything about Boston’s pricing tiers. Inner-city single-family homes are a different market entirely from condos in the outer neighborhoods. Buyers who treat “Boston” as a single price point are setting themselves up for sticker shock or missed opportunities.

Does the Math Work for Investors?

Net operating income for Boston’s multifamily sector rose approximately 6.4% in the year ending November 2024. That’s a solid number. But the picture splits when you look at property class. Class B and C properties (older buildings, less flashy finishes) continue to produce reliable returns. Luxury Class A buildings, on the other hand, are offering more concessions to fill units. If you’re buying for cash flow, the unglamorous stuff is where the math actually works.

Something most investment articles won’t say: buying a two- or three-family in Boston and living in one unit (“house hacking”) is still one of the smartest entry points into this market. You get owner-occupant financing rates, your tenants cover a chunk of your mortgage, and you build equity in a city where home values have roughly doubled since the late 2000s.

Which Boston Neighborhoods Should You Actually Consider?

Every neighborhood guide online lists the same seven areas with the same fluffy descriptions. Here’s what I’d actually tell a client sitting across from me.

| Neighborhood | Median Price | Best For | Transit | Watch Out For |

| Back Bay | $1.2M+ | Lifestyle buyers | Green/Orange | HOA fees on brownstones can top $1,500/mo |

| South Boston | ~$890K | Young pros, investors | Red Line | Flood zone exposure near waterfront |

| South End | $1M+ | Lifestyle + long-term hold | Orange Line | Victorian maintenance costs are real |

| Bay Village | ~$1.23M | Quiet city living | Walk to all | Tiny inventory; few listings per year |

| Dorchester | ~$675K | Value + growth | Red Line | Block-by-block variation in quality |

| Chinatown/Leather | ~$950K | Walkable urban | Multiple lines | Small units; limited parking |

| Roxbury | ~$650K | Investors, first-timers | Orange/Bus | Pockets still in transition |

Back Bay

Brownstones, the Charles River Esplanade, and some of the highest price tags in the city. This is where you buy if you want character, walkability, and prestige. Expect prices starting north of $1.2 million. But here’s the thing nobody mentions: the HOA fees and special assessments on older Back Bay buildings can be brutal. I’ve seen $1,800/month HOA charges that don’t even include parking. Always request three years of condo association financials before you make an offer.

South Boston

“Southie” flipped from working-class to trendy about a decade ago, and prices reflect that. The median sits around $890,000. Young professionals and investors considering rental income both find good options here, especially with Red Line access and waterfront dining. The risk factor? Flood zones. Properties near the waterfront carry increasing insurance costs as climate models get updated. Ask about FEMA zone designations before you fall in love with that water view.

South End

Victorian townhouses and converted lofts in a neighborhood known for restaurants and galleries. Average home values top $1 million. This is a long-term hold neighborhood, not a flip. The older housing stock means higher maintenance (roof, boiler, windows all cost more on century-old buildings), but the area has shown consistent appreciation for over a decade.

Bay Village

One of the smallest neighborhoods in the city. Quiet, brick-lined streets tucked between Back Bay and the Theater District. Home values average $1.23 million. The catch: inventory is almost nonexistent. Some years, fewer than 20 properties change hands here. If you want Bay Village, you need to be patient and ready to move fast when something lists.

Dorchester (North and South)

The most affordable entry point into Boston proper, with homes starting around $675,000. Dorchester is massive and wildly varied. One block might feel like suburban charm; the next might feel different entirely. Do your homework on specific streets, not just zip codes. Infrastructure investment is ongoing, and long-term growth potential is real for buyers who do the research.

Chinatown and Leather District

Close to South Station and Downtown Crossing, these areas attract people who want walkable city living and easy transit access. Home values hover around $950,000. Demand stays strong because of proximity to Boston’s financial and tech hubs. Units tend to be smaller, and parking is scarce. If you’re car-dependent, look elsewhere.

Roxbury

Median prices around $650,000 make Roxbury one of Boston’s best value plays. Urban renewal projects and a growing creative community are shifting the area’s profile. For first-time buyers and investors who want to balance city access with upside potential, Roxbury is worth a serious look. But go in with realistic timelines. Appreciation here is a five-to-ten year story, not a flip.

Is Buying Property in Boston a Good Investment in 2026?

Yes, with a caveat: it depends entirely on your buy box and your timeline. Boston is not a quick-flip market. Transaction costs (roughly 1.25–2.44% in closing costs alone) plus Massachusetts transfer taxes mean you need to hold for at least three to five years to come out ahead after selling costs.

The FRED Boston House Price Index shows that local home values have roughly doubled since the late 2000s. That kind of appreciation smooths over a lot of short-term rate anxiety. And unlike Sun Belt cities that saw volatile post-pandemic price swings, Boston’s market has stayed remarkably steady. The Harvard Joint Center for Housing Studies flagged Boston’s economy (education, life sciences, finance, tech) as a structural advantage that keeps housing demand durable even during national downturns.

For rental investors, the math pencils out best in Class B and C properties in neighborhoods like Dorchester, Roxbury, and parts of East Boston. Luxury rentals are slowing. If you’re buying a $1.5 million condo expecting 5% cash-on-cash returns, you’ll be disappointed. But a well-located two-family in a growing neighborhood? That’s a different story.

One thing the market doesn’t forgive: skipping the inspection to win a bid. Older Boston homes frequently hide $15,000 to $50,000 in first-year repair surprises (foundation issues, outdated plumbing, knob-and-tube wiring). That cost exceeds most closing cost budgets. Pay the $500 for a proper inspection. Every time.

How Does the Buying Process Work in Boston?

The process follows Massachusetts law, which is more buyer-friendly than many states. Here’s how it plays out, step by step.

1. Set Your Budget and Financing

Figure out whether you’re paying cash or financing. If financing, get pre-approved before you start touring. In Boston’s competitive market, sellers won’t take an offer seriously without a pre-approval letter. Budget for the full picture: purchase price plus 1.25–2.44% in closing costs, plus property taxes at $12.40 per $1,000 of assessed value (FY2026 rate, up 13% from last year).

2. Hire a Buyer’s Agent

After the 2024 NAR settlement, buyer-agent commissions are no longer automatically paid by sellers through the MLS. You’ll sign a written agreement disclosing and negotiating fees upfront. Typical buyer-agent rates have settled around 2–2.5%. A good agent earns that fee in a market this competitive. A bad one costs you more than their commission in missed opportunities and bad advice.

3. Get a Real Estate Attorney

Massachusetts is an attorney state. Your lawyer handles title searches, reviews contracts, explains contingencies and escrow, and protects your interests at the closing table. Expect to pay around $3,000. It’s non-negotiable. I’ve seen buyers try to skip this step to save money, and it almost always costs them more down the road.

4. Make an Offer and Sign the Purchase Agreement

Your agent submits a written offer. If accepted, you sign a purchase and sale agreement and put down earnest money (typically 5–10% of the price) into an escrow account. The contract will include contingencies for inspection and financing. In hot neighborhoods, sellers sometimes push buyers to waive contingencies. My advice: don’t. The $500 inspection is cheap insurance against a $40,000 foundation problem.

5. Due Diligence: Inspections, Title, and Appraisal

You’ll commission a home inspection and, if financing, an appraisal. Your attorney runs a title search to confirm there are no liens or legal issues. If problems surface, you can renegotiate or walk away within the contingency window. Boston’s older housing stock makes inspection especially important. Ask about the age of the roof, the boiler, the electrical panel, and any history of water intrusion.

6. Lock Your Financing

With rates in the high-6% range, locking your rate at the right moment matters. Talk to your lender about float-down options in case rates dip between contract signing and closing. If you’re buying with cash, wire instructions will come through your attorney. Triple-check those instructions. Wire fraud is a real and growing risk in real estate transactions.

7. Close the Sale

Closing usually happens 30–60 days after you sign the purchase agreement. Your attorney coordinates with the escrow agent, finalizes documents, transfers funds, and records the title. Once it’s recorded, you get the keys. Remote closings are possible through power of attorney, which is especially useful if you’re relocating from out of state.

Take Your Next Step

Boston rewards buyers who do their homework and move with confidence. The market is stabilizing, inventory is rising, and 2026 offers more breathing room than buyers have had in years. But it’s still one of the priciest markets in the country, and the penalties for cutting corners are steep. If you’re thinking about buying property in Boston and want to understand your options, working with professionals who know this specific market makes the difference between a smart purchase and an expensive lesson.

New England Home Buyers can help you understand your options, whether you’re a first-time buyer, an investor, or someone looking to make a move in a market that doesn’t slow down. Working with an experienced team that understands your market is the fastest way to avoid the mistakes that cost Boston buyers thousands every year.

FAQs

Is 2026 a good time to buy property in Boston?

For prepared buyers, yes. Inventory rose approximately 17% between September 2024 and 2025 (Greater Boston Housing Report Card), and metro median prices dipped 6.2% per Redfin’s February 2026 data. Mortgage rates in the high-6% range are actually close to the 50-year average of 7.73%. The market has more options and less frenzy than any point since 2019.

How much are property taxes in Boston for a typical home?

The FY2026 residential property tax rate is $12.40 per $1,000 of assessed value, approved by the Boston City Council in December 2025. That’s up from $11.58 in FY2025, roughly a 13% effective increase for many single-family homeowners. On an $800,000 home, you’d pay about $9,920 annually.

What are realistic closing costs when buying property in Boston?

Expect 1.25% to 2.44% of the purchase price. On a $900,000 home with 20% down, that works out to roughly $11,250 to $21,960. The biggest line items are attorney fees (around $3,000), title insurance (approximately $6,250 combined), and lender fees if you’re financing. The statewide average is about 2.44% according to Rocket Mortgage data (February 2026).

Do I need a buyer’s agent after the NAR settlement changes?

You’re not required to use one, but it’s still a smart move in Boston’s competitive market. The 2024 NAR settlement changed how agents get paid (you now negotiate directly rather than the seller paying through MLS), with typical buyer-agent rates around 2–2.5%. A skilled agent brings local knowledge, negotiation experience, and access to off-market listings that most buyers can’t find on their own.

What is the most affordable neighborhood for buying property in Boston?

Roxbury and Dorchester offer the lowest entry points inside city limits, with median prices around $650,000 and $675,000 respectively. Both are well below the citywide median of $837,000. Roxbury in particular is seeing urban renewal investment, though appreciation timelines run five to ten years rather than the quick returns some buyers expect.

How long does the buying process take in Boston?

Most purchases close within 30 to 60 days from the accepted offer. That timeline includes the inspection period (typically 7–10 days), attorney review, appraisal, and fund transfers. Cash buyers can sometimes close in as few as two weeks. Remote closings using power of attorney are available for out-of-state buyers.

Should I buy a condo or a single-family home in Boston?

Condos offer a lower entry price (median ~$866,000 in Boston proper vs. $1.31 million average for single-family). But condos come with HOA fees, special assessment risk, and less control over building decisions. Single-family homes, especially multi-family conversions, give you more flexibility and often better long-term returns. The right choice depends on your budget, risk tolerance, and whether you plan to rent units.