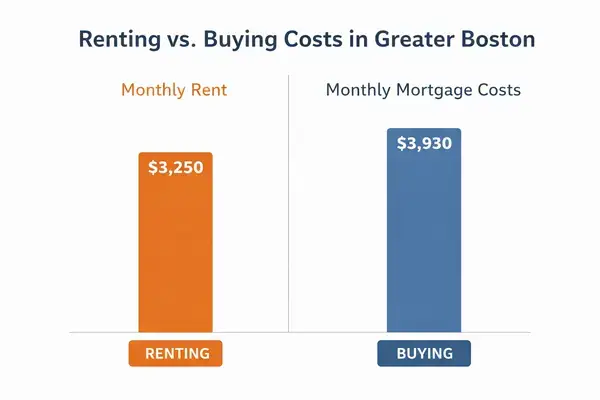

For most people in Greater Boston right now, renting is cheaper month to month than buying. That’s the short answer. The median single-family home in the metro area costs about $742,000 (The Boston Foundation, 2025), and monthly ownership costs on that property run roughly $4,500 to $5,500 once you add the mortgage, taxes, insurance, and maintenance. A comparable rental sits around $3,000 to $3,700 per month. So renting saves you $800 to $1,500 every single month in year one.

Renting vs. buying a home in Greater Boston depends on your timeline, income, and tolerance for risk. If you plan to stay at least five to seven years, buying builds serious equity in a market where prices rose 6.8% in 2024 alone (Harvard JCHS, 2025). If you might move within three years, renting almost always wins on pure math.

But monthly cost isn’t the whole picture. I’ve worked on dozens of content campaigns for real estate clients across New England, and the same mistake keeps showing up. People compare rent to a mortgage payment and stop there. They ignore property taxes, insurance spikes, the $30,000 to $80,000 in surprise repairs that Boston’s century-old housing stock loves to throw at new owners, and the opportunity cost of a six-figure down payment. This article breaks down all of it.

What this piece won’t cover: investment property analysis for out-of-state buyers, commercial real estate, or anything south of the Route 128 belt that isn’t part of the Greater Boston metro. We’re focused on the decision facing someone who lives or wants to live here.

Boston Housing Market in 2026: Prices, Rents, and Rates

The Greater Boston housing market is expensive by any measure. But “expensive” doesn’t tell you much. The numbers below put a dollar figure on what that actually means for your monthly budget, whether you rent or buy.

How Much Does It Cost to Rent in Boston Right Now?

Boston rents sit among the five highest in the country. The Zillow Observed Rent Index for the Boston metro area hit nearly $3,000 per month in late 2025 (The Boston Foundation, Greater Boston Housing Report Card 2025). Within the city limits, the numbers climb higher. Most 2025 data sources, including Zillow, RentCafe, and BostonPads, cluster Boston average rents between $3,300 and $3,690 per month.

For comparison, the national average asking rent for professionally managed apartments was $1,830 per month in Q1 2025 (Harvard Joint Center for Housing Studies, 2025). Boston renters pay roughly 80% more than the national figure.

Rent growth has cooled slightly. Annual increases dropped from the 8 to 10% spikes of 2021 and 2022 to more modest gains of 1 to 3% in 2024 and 2025. But don’t mistake slower growth for affordability. Over half of Greater Boston renters spend more than 30% of their income on housing, and over 25% spend more than half (The Boston Foundation, 2025 ACS data). That’s a cost burden most financial advisors would call unsustainable.

Vacancy rates haven’t helped. Boston’s rental vacancy has hovered near 1% in recent years. With roughly 25,000 new rental units forecast over the next three years according to HUD’s Boston Housing Market Analysis (May 2024), some relief may be coming. But new supply tends to be luxury product first, which takes years to filter down to market-rate affordability.

What Are Boston Home Prices Doing in 2026?

The median single-family home in Greater Boston sold for $741,738 in the first half of 2025 (The Boston Foundation, 2025). Boston proper was even higher at $837,287. The median condo came in at $721,852.

To put that in perspective, the national median existing single-family home sold for $412,500 in 2024 (Harvard JCHS, 2025). Greater Boston runs about 80% above that national figure.

The Northeast region posted the strongest price growth of any part of the country in 2024 at 6.8% year over year (Harvard JCHS, 2025). Prices across the Northeast have climbed a staggering 68% since 2019. National prices rose about 60% over that same window. So Boston isn’t just expensive. It’s getting more expensive faster than most of the country.

Here’s a contrarian take most articles skip: that rapid appreciation is great if you already own. If you’re trying to buy, it means every year you wait costs you roughly $40,000 to $55,000 in additional purchase price on a median home. The math on “wait and save more” doesn’t work when prices move that fast. I’ve seen this pattern play out with real estate clients across the region, and the renters who waited from 2020 to 2025 are now priced into a completely different tier.

Where Do Mortgage Rates Stand?

Thirty-year fixed mortgage rates sat in the mid-to-high 6% range through most of 2025. That’s a far cry from the 2.7 to 3% rates that buyers locked in during 2020 and 2021. But it’s worth remembering that the 50-year historical average for a 30-year mortgage is about 7.7%. Today’s rates feel high only compared to an abnormal two-year window that spoiled an entire generation of buyers.

What higher rates actually mean in dollars: on a $742,000 home with 20% down ($593,600 loan amount), the difference between a 3% rate and a 6.5% rate is roughly $1,400 per month in extra interest. That’s real money. It pushes many would-be buyers out of the market entirely. And it’s the primary reason why homebuying nationwide dropped to its lowest level in decades according to Harvard’s 2025 housing report.

Some buyers are holding out for rate drops. Maybe they’ll come. Maybe they won’t. But if rates drop to 5.5%, home prices will almost certainly jump because more buyers flood back in. You don’t get lower rates AND lower prices. Pick one. My advice to clients’ audiences has always been the same: buy at today’s price, refinance at tomorrow’s rate.

Can the Average Boston Household Afford to Buy?

This is where the data gets uncomfortable. The income required to buy a starter home in Greater Boston (5th to 35th percentile price tier) is now $162,224 per year. That assumes a 3.5% down payment, 30-year fixed rate, and staying within a 31% debt-to-income ratio (The Boston Foundation, 2025). For the median-priced single-family home, you need roughly $236,000 in household income (Boston Globe analysis of TBF data, December 2025).

That’s a problem. Only 15% of Greater Boston renter households, about 114,000 families, can afford an entry-level home today. That number was 30% (213,000 households) in 2021. The share of renters who can afford to buy has been cut in half in just four years according to The Boston Foundation’s 2025 report.

The price-to-income ratio in Boston sits around 8.3x, meaning the median home costs 8.3 times the median annual household income. The national average is closer to 4.7x. Boston ranks among the 10 least affordable large cities in the country by this measure.

Renting vs. Buying: Monthly Cost Comparison (Greater Boston 2026)

| Cost Category | Renting (Median) | Buying (Median SFH) |

| Monthly Payment | $3,300–$3,700 rent | $3,750 (P&I on $593k @ 6.5%) |

| Property Taxes | $0 (included in rent) | $800–$1,300/month |

| Insurance | $25–$50 renters insurance | $200–$400/month |

| Maintenance/Reserves | $0 | $600–$750/month (1% rule) |

| Total Monthly Cost | $3,325–$3,750 | $5,350–$6,200 |

| Equity Built (Year 1) | $0 | ~$8,500–$10,000 |

| Upfront Cash Needed | $6,600–$11,100 (first/last/deposit) | $26,000–$148,000+ (3.5–20% down + closing) |

Sources: The Boston Foundation 2025 Report Card, Harvard JCHS 2025, HUD Boston HMA 2024. Mortgage assumes 20% down, 30-year fixed at 6.5%. Property tax estimate uses ~2.1% effective rate common in Greater Boston suburbs.

Does Buying a Home in Boston Actually Save You Money?

Short answer: yes, if you stay long enough. The breakeven period in Greater Boston is five to seven years minimum, and closer to seven to ten years when you factor in today’s tax rates, insurance costs, and the maintenance surprises that come with Boston’s older homes (multiple 2025 and 2026 realtor analyses citing TBF data, NAR breakeven rules for high-cost metros).

Monthly Costs: Renting vs. Owning Side by Side

The table above makes it clear. Renting a comparable home in Greater Boston runs $1,500 to $2,400 less per month than owning. That gap is wider than most rent-vs.-buy articles admit, because most articles ignore property taxes and maintenance. Massachusetts effective property tax rates average around 2.1% in many suburban towns, which adds $800 to $1,300 per month on a median-priced home. National homeowner insurance premiums jumped 57% between 2019 and 2024 (Harvard JCHS, 2025). That’s not a typo. Fifty-seven percent in five years.

And then there’s the cost nobody budgets for. Boston’s housing stock is old. Really old. Triple-deckers from the 1920s, colonials from the 1940s, split-levels from the 1960s. Contractors and realtors in local forums consistently report that new owners face $30,000 to $80,000 in surprise repairs during their first three to five years. Roof replacements, boiler failures, window upgrades, lead paint abatement. No home inspector catches all of it.

What About Building Equity?

Equity is the main financial argument for buying, and it’s a strong one. Nationally, homeowners have a median net worth around $400,000 compared to about $10,400 for renters (Federal Reserve Survey of Consumer Finances). That’s a 38x difference. Some of that is selection bias (higher-income people buy more often), but most of it comes from forced savings and appreciation.

In Greater Boston, homes appreciated 6.8% in the Northeast region during 2024 and 68% since 2019. If you bought a $600,000 home in 2019, it’s worth roughly $1,008,000 today. That’s $408,000 in appreciation alone, plus whatever you paid down on the mortgage. No stock portfolio guarantees that kind of return on a leveraged asset.

The counterargument: if a renter invested that $148,000 down payment into a diversified index fund returning 8% annually, they’d have about $217,000 after seven years. That’s solid. But it requires discipline that most people don’t have, and it doesn’t provide housing. You still pay rent while your investments grow. When I compare the two paths for clients exploring their real estate options, ownership wins for anyone staying seven or more years in this market.

How Long Before Buying Beats Renting?

The general rule from the National Association of Realtors and most financial advisors: five to seven years in high-cost metros. But in Greater Boston circa 2026, the real breakeven is closer to seven to ten years. Why longer than the national rule? Three reasons.

First, upfront costs are enormous. Closing costs plus down payment on a $742,000 home easily total $50,000 to $175,000. That money has to be recouped through appreciation and equity before ownership “wins.” Second, property taxes in MA are among the highest in the Northeast. Third, insurance and maintenance costs have spiked since 2020.

If you plan to stay 10+ years? Buying is a no-brainer in Greater Boston. Five to seven years? It’s a toss-up that depends on appreciation rates, your tax bracket, and what you’d do with the down payment otherwise. Less than five years? Rent. Don’t even debate it. The transaction costs of buying and selling a house in Massachusetts will eat any equity you build.

Who Should Rent and Who Should Buy in Greater Boston?

The right choice depends less on what the market does and more on where you are in life. A 26-year-old software engineer and a 65-year-old empty nester should be running completely different calculations.

Young Professionals and First-Time Buyers

If you’re in your twenties or early thirties and working in Boston’s tech, biotech, or healthcare sectors, renting is probably your best move right now. Not because it’s “smarter,” but because the math is brutal for first-time buyers. You need $162,224 in household income just for a starter home. That’s a senior engineer’s salary, not an entry-level one.

About 25% of millennials in 2022 said they plan to always rent, nearly double the share from a few years earlier (Money.com survey). The top reasons: they can’t afford to buy, they value flexibility, and they don’t want maintenance headaches. In Boston, all three of those reasons carry more weight than in cheaper markets.

But if you’ve saved aggressively and plan to stay in Boston five or more years, buying a condo can make sense. A two-bedroom condo in Somerville or Malden is more reachable than a single-family home, and you start building equity immediately. Some young buyers rent out a spare room to offset costs, which works well in a city full of graduate students and traveling medical professionals.

Worth noting: Massachusetts’ first-time homebuyer assistance programs can help with down payment and closing costs. MassHousing and ONE Mortgage programs offer below-market rates and reduced down payments for qualifying buyers. Not enough people know about these.

Growing Families Looking for Space

Families with kids tend to lean toward buying, and for good reason. Stability matters when you’re picking school districts. You can’t renovate a rental. And renting a three-bedroom single-family home in a good suburb runs $4,000 or more per month anyway, which starts to close the gap with ownership costs.

The classic family move in Greater Boston: sell the city condo (or leave the city rental), buy in Newton, Lexington, Winchester, or Needham. These suburbs have strong schools and have delivered consistent appreciation. They’re also painfully expensive. A four-bedroom colonial in Needham will run you well over $1 million.

One strategy that’s worked for families I’ve seen profiled in campaigns across the region: buying a two-family or three-family property instead of a single-family. You live in one unit and rent the other. A couple in Watertown, for example, purchased a two-family and the rental income covered a huge chunk of their mortgage (Boston Globe reporting). They went from paying someone else’s mortgage to building their own equity. For families willing to be landlords, multifamily properties in towns like Watertown, Waltham, or Malden offer a path that pure single-family purchases can’t match.

Retirees and Empty Nesters

If you’ve owned a home in Greater Boston for 20 or 30 years, you’re sitting on a goldmine. A home purchased for $300,000 in 2000 might be worth $900,000 to $1.3 million today. The question is what to do with that equity.

Some retirees sell and rent, unlocking hundreds of thousands in cash to fund retirement. A $4,000 per month rental in Brookline is a lot. But if you sold a $1.2 million home and invested the proceeds conservatively at 4 to 5%, that portfolio generates $48,000 to $60,000 annually. That covers rent with room to spare, and you never replace another roof or furnace.

Others downsize to a smaller condo, keeping the tax advantages of ownership while shedding the maintenance burden. A 55+ community condo in the $400,000 to $600,000 range offers a middle path.

The risk of renting in retirement: rent increases don’t stop. If you live another 20 years, that $4,000 rent at 3% annual increases becomes $7,200. Your investment portfolio needs to keep pace. For retirees who want certainty, owning a paid-off condo offers a fixed cost that renting can’t match. If your situation is complex, selling for cash and simplifying your living arrangement might be the right first step.

How Can You Make Boston Homeownership More Affordable?

Boston’s prices scare people off. But there are strategies that change the math. Some of these are common knowledge. A few are underused and underreported.

House Hacking with Multi-Family Properties

House hacking is the single best financial move a first-time buyer can make in Greater Boston. Buy a two-family or three-family, live in one unit, rent the rest. FHA loans let you do this with as little as 3.5% down on a property with up to four units, as long as you live in one.

The math on a three-family in Somerville: purchase price $1.1 million. Your unit is one of three. The other two units rent for $2,400 each, bringing in $4,800 monthly. Your total PITI is around $7,200 per month. After rental income, your out-of-pocket cost drops to $2,400. That’s less than renting a one-bedroom in the same neighborhood.

There are trade-offs. You’re a landlord. You deal with tenants, repairs, and the occasional 2 AM plumbing call. But the financial upside is massive. You’re building equity on a $1.1 million asset while paying less than a renter. I’ve seen this strategy turn 30-year-olds into millionaires by their mid-forties. It works especially well in Boston’s triple-decker neighborhoods.

Short-Term Rentals and the New ADU Law

Two big developments changed the calculus for Boston-area homeowners in 2025.

First, the Massachusetts Affordable Homes Act (Chapter 150 of 2024) went into effect on February 2, 2025. It allows one accessory dwelling unit up to 900 square feet on most single-family lots statewide, by right, with no special permit required. That means if you buy a single-family home with a detached garage or a large basement, you may be able to add a rental unit. The ADU won’t lower your purchase price, but it creates a new income stream that didn’t exist before 2025.

Second, short-term rentals (Airbnb, VRBO) remain legal in Boston for owner-occupied properties. You must live on-site at least nine months of the year. If your property qualifies, renting a spare room or an in-law unit during peak periods (graduation season, marathon weekend, leaf season) can generate significant income. Just know that Boston’s regulations are strict, and suburbs have their own rules.

The Live-In Flip Strategy

Boston’s older housing stock actually creates an opportunity here. Buy a dated home in a strong neighborhood at a relative discount. Live in it for two or more years while making targeted improvements. Then sell and pocket up to $250,000 in tax-free gains ($500,000 for married couples) under the primary residence capital gains exclusion.

The risk: renovation in Boston is expensive, slow, and heavily regulated. Permitting alone can add months to a project. But for buyers with some renovation tolerance, the potential return is real. A $50,000 kitchen and bath renovation on a $700,000 home in a neighborhood where comps sell for $850,000 is a play that pencils out. You’re just not going to know your exact capital gains tax exposure until the sale closes.

Co-Buying and Alternative Paths

Co-buying is growing in high-cost markets. Two friends or siblings buy a two-family together, each taking a unit. You split the down payment, split the mortgage, and each build equity on half the property. It requires a solid legal agreement (hire a real estate attorney), but it cuts the barrier to entry in half.

For people who want real estate exposure without owning their primary residence, REITs and real estate crowdfunding platforms offer a middle ground. You rent your home and invest in the asset class through markets instead. It’s not the same as owning, but it keeps your money working while you stay flexible.

Real Scenarios: How the Math Plays Out

Numbers tell the story better than opinions. Here are four profiles that represent the most common situations I see across the Greater Boston market.

Scenario 1: The Young Tech Worker (Renting)

Age 29. Single. Earns $135,000 at a Cambridge biotech firm. Rents a one-bedroom in Davis Square for $2,600 per month. Has $45,000 in savings. To buy a comparable condo at $550,000 with 10% down, he’d need about $55,000 for down payment plus closing costs and face monthly PITI of roughly $4,100 (before maintenance and HOA fees). His rent is $1,500 less per month. He invests the difference in index funds. After five years, his portfolio grows to roughly $120,000 to $140,000 assuming 7 to 8% returns. Meanwhile, a condo purchased at $550,000 appreciating at 5% per year is worth $702,000, with about $80,000 in principal paid down. The condo buyer is ahead by roughly $100,000 to $150,000 in net wealth. But the renter retained mobility and avoided the risk of a $20,000 special assessment.

Scenario 2: The House-Hacking Couple (Buying)

Ages 34 and 36. Combined income $180,000. They buy a two-family in Watertown for $950,000 with 10% down ($95,000). They live upstairs and rent the downstairs unit for $2,600. Total PITI plus insurance and maintenance: roughly $7,000 per month. After rental income, their out-of-pocket cost is $4,400. Their old Cambridge apartment cost $3,200 in rent. So they’re paying $1,200 more per month, but building equity on a $950,000 asset. After five years at 5% appreciation, the property is worth $1,213,000. They’ve built roughly $330,000 in equity (appreciation plus principal paydown). If they’d kept renting, they would have spent $192,000 in rent with zero equity.

Scenario 3: The Suburban Family (Buying, Stretched)

Mid-thirties. Two kids. Household income $220,000. They buy a $1.05 million colonial in Needham with 15% down. Monthly costs: roughly $7,800 including mortgage, taxes, insurance, and maintenance reserves. That’s 42% of gross income, which is above the recommended 28 to 31% threshold. Year one is tight. They skip vacations and eat out less. After seven years, the home appreciates to roughly $1.48 million (5% annual growth). They’ve accumulated about $530,000 in equity. The salary needed to buy a home in Boston keeps climbing, but their locked-in mortgage doesn’t.

Scenario 4: The Downsizing Retiree (Selling, Then Renting)

Age 68. Widowed. Sells the family home in Newton for $1.3 million. Pays off the small remaining mortgage and nets roughly $1.1 million. Rents a modern one-bedroom in Brookline for $3,800 per month. Invests the proceeds in a conservative 4% yield portfolio generating $44,000 per year. Rent costs $45,600 annually, so the portfolio nearly covers it, with Social Security and pension filling the gap. No more property taxes ($12,000 per year saved), no more maintenance ($8,000 per year saved), no more snow removal headaches. The risk: rent at 3% annual increases becomes $5,100 per month in 10 years and $6,900 in 20 years. The portfolio needs to grow to keep pace.

How to Decide: Rent or Buy in Greater Boston

Forget the generic advice. Here’s the decision framework that actually works.

If you’re staying 7+ years, have 10 to 20% saved for a down payment, and can keep total housing costs below 33% of gross income: buy. The equity math is too good to ignore in a market that’s appreciated 68% since 2019. Waiting costs you more than buying at today’s rates.

If you’re staying less than 5 years, don’t have 6 months of reserves beyond your down payment, or would need to spend more than 40% of income on housing: rent. No amount of long-term equity potential justifies a financial emergency in year two when the boiler needs replacing in January.

If you’re in between, ask yourself two questions. First, what’s the biggest home repair bill you could handle right now without going into debt? If the answer is less than $25,000, you’re not ready. Second, would you take a 20% stock market loss and hold, or would you panic-sell? Owning a home is the same emotional test. If you’d sell a portfolio in a dip, you’ll panic-sell a house in a down market and lock in losses.

One last thing. The biggest expense in renting vs. buying isn’t the monthly payment. It’s the decision delay. Every year of appreciation you miss on the buy side is money you don’t get back. And every year of rent you pay is money that builds someone else’s equity. Neither path is wrong. But indecision, waiting another year “just to see,” is almost always the most expensive choice.

Renting vs. buying a home in Greater Boston comes down to your timeline, your savings, and your stomach for risk. The numbers favor ownership for long-term residents and favor renting for anyone in transition. Run your own math with real local data from trusted sources, not national averages that don’t apply here.

FAQs

How much income do you need to buy a starter home in Greater Boston in 2026?

You need a household income of roughly $162,224 to afford an entry-level home in Greater Boston, assuming a 3.5% down payment and 30-year fixed mortgage (The Boston Foundation, 2025). Only about 15% of current renter households in the region qualify at that threshold, down from 30% in 2021.

Is renting still cheaper than buying in Boston month to month?

Yes. Monthly ownership costs for a median-priced single-family home in Greater Boston (including mortgage, taxes, insurance, and maintenance) run about $5,350 to $6,200. A comparable rental costs $3,300 to $3,700. Renting saves $800 to $1,500 per month in year one. Buying catches up through equity and appreciation over five to ten years.

How long do I need to stay in a home to break even on buying vs. renting in Greater Boston?

The minimum breakeven period in Greater Boston is five to seven years, and it stretches to seven to ten years when you include Massachusetts property taxes (averaging around 2.1%), rising insurance premiums, and the maintenance costs of older housing stock. National Association of Realtors guidelines and 2025 to 2026 local analyses consistently cite this range.

What are the hidden costs of buying a home in Boston that renters avoid?

Beyond the mortgage, Boston homeowners pay property taxes ($800 to $1,300 per month on a median home), homeowner’s insurance (up 57% since 2019 per Harvard JCHS), and maintenance reserves (the 1% rule suggests $7,400 per year on a $742,000 home). Boston’s century-old housing stock frequently hits new owners with $30,000 to $80,000 in surprise repairs in the first three to five years.

Will the new Massachusetts ADU law make buying more affordable?

The Massachusetts Affordable Homes Act, effective February 2, 2025, allows one accessory dwelling unit up to 900 square feet by right on most single-family lots. This creates a new rental income stream for homeowners but does not lower purchase prices. An ADU renting for $1,500 to $2,000 per month can offset ownership costs and shorten the breakeven timeline.

Is house hacking a realistic strategy in Greater Boston?

Yes, and it’s one of the most effective. Buying a two-family or three-family property with an FHA loan (3.5% down for owner-occupants) and renting out the other units can reduce your out-of-pocket housing cost to less than local rent prices. A three-family in Somerville with two rental units at $2,400 each brings in $4,800 monthly, covering most of a $7,200 PITI payment.

What happens to renting vs. buying math if mortgage rates drop?

If rates fall to 5% to 5.5%, monthly ownership costs decrease by $400 to $600 on a median-priced Greater Boston home. But rate drops typically trigger more buyer demand, pushing prices higher. You rarely get lower rates and lower prices at the same time. Buying at current rates and refinancing later is a common strategy that preserves today’s pricing.